The US-China stand off

It is widely believed that China has dominated the growing REE industry, and that it was much quicker than the United States to understand its strategic value. By 2019 China was supplying around 90% of global demand for the 17 REE powders. It also currently controls 70% of global rare earth processing capacity.

Since as early as 2010, the Beijing government has placed restrictions on its REE exports. By 2025, when the US began a trade and tariff war with China, the US and Australia had become the world’s second and third largest REE producers. While lower down the production ranking, Brazil is also seen as an REE powerhouse, since it has the world’s second largest REE reserves.

The US was hard hit in 2025 when China imposed export restrictions on metals, machine parts, engineers, and rare earths. A one-year truce was agreed in November but by then many US and European factories had been forced to limit production levels.

What is the outlook for demand?

Across a range of mining sector analysts there is agreement that a global boom in demand for critical minerals has been taking shape in recent years. Lithium demand, based on the high-powered batteries that are needed by the world’s growing fleet of electronic vehicles (EVs), is expected to surge by 400%-500% over the next ten years. Copper use in renewable energy could jump by 300%. Achieving the UN’s global carbon net zero target by 2050 could require a six-fold increase in critical mineral inputs by 2040. The underlying economic model suggests that every US$1bn invested in upstream mining generates US$3bn-$4bn in downstream manufacturing.

It needs to be stressed that, however promising, REEs and critical minerals development in Latin America are at a very early stage and starting from a small base. It is predicted that regional REE production could grow at a compound annual rate of 7.4% in 2025-2030, but the value of production in 2030 will be only around US$32m. At the other extreme there are claims that the regional mining/refining value chain could eventually reach a value of US$154bn.

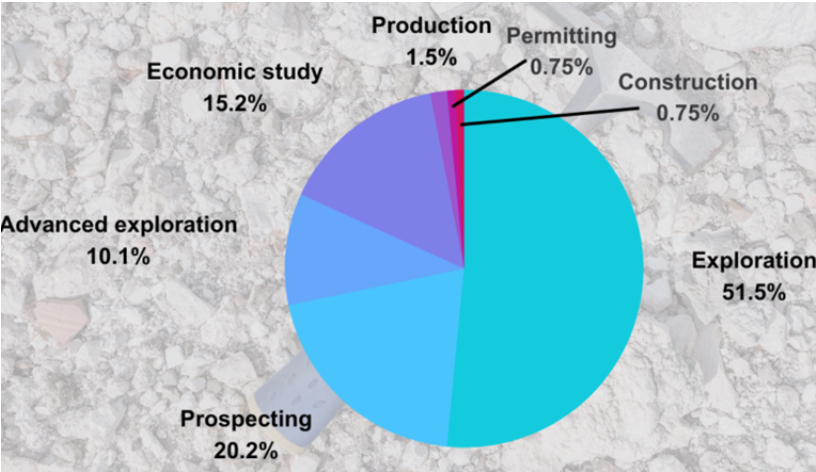

Stages of rare earths projects across the Americas

Source: The Northern Miner

Brazil, Latin America’s economic powerhouse, has set itself some super-ambitious targets. It currently accounts for 0.02% of global REE supply and wants to boost that to a 5%-8% market share by 2030, relying on integrated mining and processing. To help make that possible it has promised the equivalent of US$500m in investment in transport infrastructure, including railways and ports.